How Do I Launch a Direct Primary Care + HRT Subscription Without Dropping Insurance? (The Cash-Pay Build-Out Playbook)

Most primary care and hormone practices think going cash-pay means burning the insurance business down and starting over. It doesn’t. The fastest, lowest-risk way to build recurring cash revenue is to layer a direct primary care and HRT subscription on top of the practice you already have — using the patients your insurance schedule can’t reach fast enough. Here’s the FAQ on how to build it out: the pricing, the sequencing, and the exact front-desk script that converts an insurance inquiry into a cash-pay member.

Can I Launch Direct Primary Care Without Dropping Insurance?

Yes — and you should. You don’t have to choose. Run a cash-only track alongside your insurance track and let each one do what it does best.

Here’s the insight most owners miss: your supply problem usually isn’t provider availability — it’s insurance provider availability. Credentialing a provider with payers takes at least 60 days, and your insured new-patient schedule may already be booked two to three weeks out (often six to eight weeks in practice). But a provider can see self-pay patients almost immediately, because cash visits don’t require payer credentialing at all. They just need to be added to malpractice coverage.

That gap is the opportunity. Every patient who can’t get an insurance appointment for six weeks is a patient you can see this week — for cash. Build a cash-only track to absorb that overflow, and you’ve created a new revenue line without touching your existing insurance business. Concierge and DPC practices already operate exactly this way: cash for access to the provider, insurance for everything else.

How Fast Can a New Provider Start Seeing Cash-Pay Patients?

Almost immediately — payer credentialing doesn’t apply to cash, so a new provider can be booking self-pay visits within days of being added to your malpractice policy.

This is the unlock that makes the whole model low-risk. You don’t have to wait 60-plus days for credentialing to come back before that provider generates revenue. Start them on cash-only shifts the moment they’re covered. One clinic we worked with had a new provider starting on the 20th and could offer its first cash-pay opening for early the following month — well before any insurance credentialing would have cleared.

Don’t over-hire on day one. Begin with a single extra cash-only shift on the schedule, prove the demand over about six weeks, and only then commit to a dedicated cash-only provider. You’ll know the demand is real before you’ve added a fixed cost.

Should I Charge a Monthly Subscription or Fee-for-Service for Direct Primary Care?

Do both. Price the standalone visit so it’s profitable on its own, then offer a subscription on top — but only to the patients it actually fits.

The standalone visit has to stand alone. If a patient never subscribes, the visit you sold them should still be a profitable transaction. Then, for the patients who want ongoing hormone therapy, peptides, or regular access, the subscription is the upsell — and it’s where the real value is, because recurring revenue is predictable, compounds, and is far easier to forecast and reinvest than one-off visits.

The mistake is pitching the subscription to everyone. A patient who came in for one acute issue and has no interest in hormones doesn’t need a membership, and pushing it makes you look like you’re selling instead of helping. Reserve the subscription for the patients whose needs are genuinely ongoing.

An HRT clinic we grew from $1M to $4M a year built a large share of that on recurring memberships — that’s the durability a subscription adds that fee-for-service never will.

What Should I Charge for DPC Visits and an HRT Membership?

For the visits, roughly $200 for an initial without labs, $250 with labs, and $100 for follow-ups. For the membership, around $275 a month — and benchmark it against your local concierge competition.

Those visit prices are what one clinic landed on as it moved off a too-cheap self-pay rate. The membership at about $275 a month works out to roughly $3,300 a year, which you can position directly against local concierge pricing — in that market, a concierge MD charged $3,000 a year and an NP $1,800 a year.

To clearly out-value them, bundle real benefits into the membership:

- Labs included

- Discounts on hormones

- Peptides

- Supplements

- Sick visits included for kids

The point of the bundle is that the member never feels nickel-and-dimed. Every lab, every quick visit, every refill that would otherwise be a separate charge is folded in. That’s what makes a member stay — and what makes the math obviously better than the concierge clinic down the road that charges more and includes less.

How Do I Explain Direct Primary Care to a Patient Who Already Has Insurance?

Tell them they keep their insurance — for labs, imaging, and prescriptions. They’re only paying cash for one thing: fast, direct access to the provider.

This reframe removes the biggest objection. Patients hear “cash-pay” and assume they’re paying for everything out of pocket. They’re not. The DPC model is “keep your insurance for your labs, your imaging, your prescriptions” — the cash buys access and time with the provider, not the downstream care.

Many insured patients already do exactly this when their plan is poor or not accepted: they pay the self-pay visit rate and run their labs through Quest on their own insurance.

And here’s the part that closes it: once you factor in co-pays and the labs they’d pay for anyway, cash-pay patients sometimes spend less out of pocket than they would going through insurance — while getting in this week instead of in six. When you can say that honestly, the cash option stops feeling like a downgrade and starts feeling like the smart choice.

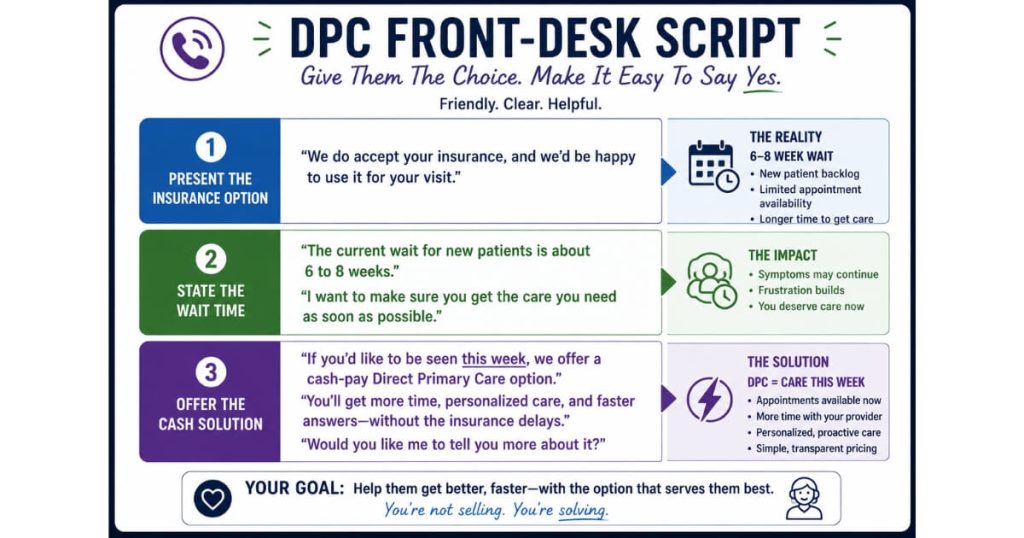

What Should My Front Desk Say When a Patient Asks About Appointments?

Present the insurance option first, tell them the real wait, then offer the cash-pay solution as the fast alternative — and let them choose.

The sequence matters. If you lead with cash, it sounds like you’re upselling. If you lead with insurance and let them feel the six-to-eight-week wait themselves, the cash option becomes the obvious relief.

The script sounds like this:

“I can get you on the schedule with insurance, though our next new-patient opening is about six weeks out. What we’ve found is that, once you factor in co-pays and labs, our cash-pay patients are sometimes paying even less out of pocket — and as a new cash-pay patient on our direct primary care model, I could get you in this week. Which would you prefer?”

Then role-play it. Don’t just hand the team a script — sit down and run the call until it sounds natural, because a script read stiffly converts worse than no script at all. Build an intake form so any inbound that wants the cash option flows straight into your CRM, and the front desk never has to do double data entry to book it.

When Should I Raise My Cash-Pay Prices?

Gradually — the “boiling pot” approach. Start lower to fill the schedule, then raise prices roughly every six weeks as demand proves out.

Get patients in the door at a price that’s easy to say yes to, then increase it in steps as the calendar fills. Re-evaluate about every six weeks: if you’re booking out, raise again. A comparable clinic did exactly this — it raised prices in the spring and nearly doubled its monthly membership from under $200 to $300 and $350, with or without hormones, and ended up booked out for months with plans to raise again. The market tolerated every increase because demand kept proving it could.

Owners almost always underprice cash-pay care out of fear. The boiling-pot method removes the fear: you’re never making a scary one-time jump, just a series of small, demand-justified increases.

This is also how a practice transitioning off insurance protects its cash flow — much like Dr. Groysman, who cut insurance dependence in half and added more than $40K a month by moving deliberately toward cash rather than all at once.

FAQs About Launching a DPC + HRT Subscription

Do I Have to Drop Insurance to Start a Direct Primary Care Model?

No. Run a cash-only track alongside your insurance track. Cash visits don’t require payer credentialing, so a provider can see self-pay patients almost immediately and absorb the overflow your insurance schedule can’t reach for weeks.

What Should I Charge for a DPC Membership?

Around $275 a month (roughly $3,300 a year) works when benchmarked against local concierge pricing and bundled with real value — labs included, discounts on hormones, peptides, and supplements, and kids’ sick visits. Price your standalone visits ($200 without labs, $250 with, $100 follow-ups) to be profitable even if the patient never subscribes.

How Do I Pitch DPC to a Patient Who Has Insurance?

Tell them they keep insurance for labs, imaging, and prescriptions and only pay cash for fast, direct access to the provider. Once co-pays and labs are factored in, many patients pay less out of pocket on cash-pay while getting in this week instead of in six.

Should I Offer the Subscription to Every Patient?

No. Reserve the membership for patients with ongoing needs — hormones, peptides, regular access. Pitching a subscription to a one-time acute patient makes you look like you’re selling rather than helping.

When Should I Raise My Cash-Pay Prices?

Use the “boiling pot” method: start lower to fill the schedule, then raise roughly every six weeks as demand proves out. Small, demand-justified increases let you climb to the right price without a scary one-time jump.

What’s the Next Step?

If you’re sitting on an insurance practice with a packed schedule and a six-week wait, you’re leaving recurring cash revenue on the table every single week. The build-out is straightforward: a cash-only track to absorb overflow, standalone visit pricing that’s profitable on its own, an HRT subscription for the patients with ongoing needs, a front-desk script that lets the patient choose, and a boiling-pot pricing climb.

On a strategy call we’ll map your specific build-out — what to price the visits and membership at for your market, how to sequence the launch, and the exact front-desk script for your team. We’ve helped practices make this transition without losing the patient base, including clinics that moved off insurance dependence while growing recurring revenue.